For owners of logistics and freight companies, procurement teams in construction and mining, and small business owners managing delivery fleets, understanding commercial truck insurance is crucial. The costs associated with insuring commercial trucks can vary widely based on numerous factors including vehicle size, type of coverage, and regional risk. This article will delve into the core elements that influence how much commercial truck insurance will cost, the various factors at play, and the average pricing structures observed across different categories of vehicles. By the end, readers will be better equipped to navigate this essential aspect of their operations.

Unraveling the Complex Costs: A Deep Dive into Commercial Truck Insurance Pricing Factors

Commercial truck insurance is more than just a regulatory necessity; it is a finely balanced interplay of risk management, economic strategy, and evolving market dynamics. This chapter navigates the intricate terrain of commercial truck insurance expenses by exploring the nuanced cost elements, drawing connections that are vital for fleet operators, logistics companies, and independent truck owners aiming to manage their overhead costs effectively. Each cost element, from vehicle type to driver history, plays a pivotal role in shaping the overall premium, and understanding these determinants is crucial for making informed decisions in a competitive industry.

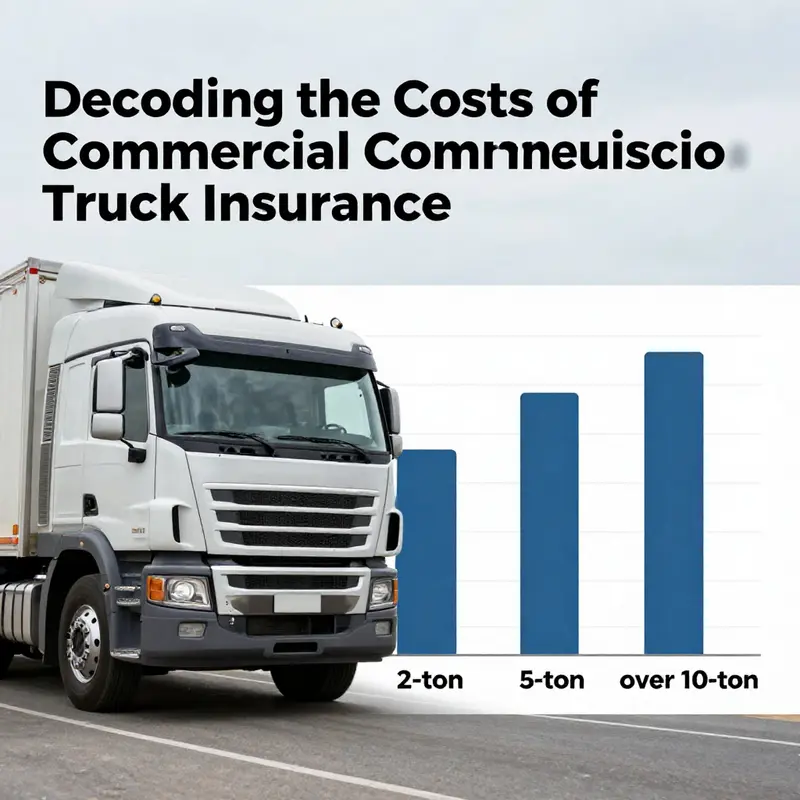

At its core, the pricing of commercial truck insurance is driven by risk assessment and potential liabilities. One cannot discuss the cost without first considering the vehicle itself. The type and size of the truck are significant variables that insurers scrutinize. For example, a 4.2-meter box truck, often deployed in urban environments for efficiency, typically attracts higher premiums than smaller cargo vans due to its increased cargo capacity and associated risk factors. Larger trucks, particularly those classified as over 10 tons, often come under even more stringent conditions due to the amplified destructive potential and the higher replacement values involved. In these cases, third-party liability coverage alone can demand premiums in the range of $5,500 to $6,000 annually. These figures serve as a baseline, upon which further adjustments are made depending on other influencing factors.

The intended use and business purpose of a vehicle add another layer of complexity to cost assessments. A truck employed strictly for personal use, such as occasional hauling during non-business hours, is typically subject to lower premiums compared to one integrated into a commercial operation. Commercial operations imply intense utilization, longer daily driving hours, and a higher probability of involvement in incidents, all of which escalate the insurer’s risk exposure. Consider a scenario where the same 4.2-meter box truck is used for private purposes versus being a staple in a logistic fleet. The premium for its commercial counterpart not only starts at a higher base but continues to escalate as additional coverages—like cargo and passenger liability insurance—are layered on. These increased risks mean that every operational detail is factored into the final premium determination, creating a tailored approach that aligns coverage with specific business needs.

Geographic location also plays a critical role in shaping premium costs. The location of the operations or even the depot where the truck is based can directly impact the risk profile. Urban centers, recognized for high traffic density, frequent congestion, and a propensity for collisions, inherently command higher premiums. In cities like Beijing or Guangzhou, where congestion can contribute to a higher frequency of minor to major claims, the resulting premiums can easily exceed $6,000 annually. In contrast, trucks based in rural or less congested regions, where accident statistics tend to be more favorable, may benefit from lower premiums. The role of regional risk is not just confined to accident rates; local insurance regulations can impose additional requirements, further complicating the cost structure. These variations emphasize the necessity for truck operators to obtain location-specific quotes, ensuring that their premium accurately reflects the underlying risk of their operational environment.

An often underappreciated yet highly influential factor is the driver’s history and the claims record maintained by both the individual and the company. Insurance providers are meticulous when reviewing past driving behavior. A history marked by multiple claims or accidents signals a higher likelihood of future incidents, prompting significant increases in the premium. In contrast, a clean driving record often results in the application of no-claim discounts, sometimes offering reductions of up to 30% on compulsory insurance portions. This incentive underlines the importance of rigorous driver training and the implementation of safety programs within fleet management, as these measures not only improve operational safety but also offer tangible cost benefits by reducing insurance premiums over time.

The coverage levels and the choice of additional addons further expand the financial landscape of commercial truck insurance. Basic packages typically combine compulsory insurance, vehicle damage insurance, and third-party liability coverage with limits that may range around a million RMB. These foundational coverages offer a baseline level of protection, but many businesses opt to include additional services that align more precisely with their operational needs. For instance, cargo insurance is critical for companies that transport high-value or sensitive goods across long distances or cross provincial borders. Similarly, vehicles carrying passengers necessitate the addition of passenger liability insurance to protect against claims arising from personal injury. The integration of temperature control equipment insurance in refrigerated trucks is another illustrative example, where the cost of coverage rises in tandem with the critical nature of the goods being transported. Each additional coverage layer does not operate in isolation; rather, it compounds the total premium. Consequently, while the basic package might be priced between ¥6,000 and ¥7,000 annually, the inclusion of multiple optional addons can noticeably drive up overall expenses.

Another significant consideration is the value and age of the vehicle. Newer trucks, by virtue of their higher replacement cost and modern technology, are often categorized as high-risk by insurers. This assessment leads to more expensive premiums, particularly under vehicle damage insurance, which can range between ¥5,000 and ¥6,000 annually for new vehicles. As trucks age, depreciation tends to lower the overall insured value, thereby reducing the cost of vehicle damage coverage. However, older vehicles may simultaneously attract higher premiums in other areas if they are more prone to mechanical issues or if they lack advanced safety features. This paradox highlights the balancing act insurers engage in: while the market value of a vehicle diminishes, the risk associated with operational reliability may conversely increase.

Market competition and the diversity of insurance provider pricing models add yet another dimension. Even when all variables remain constant, different insurers may offer varying quotes. For example, the premium for a 4.2-meter box truck might differ notably from one company to another, with pricing examples ranging from competitive offers to slightly inflated figures. This variability underscores the importance of obtaining multiple quotes tailored to one’s specific needs. Operators are well-advised to negotiate and compare offers across several reputable insurers, ensuring that they achieve not only the best price but also the most comprehensive coverage. In some instances, even established companies may have to adjust their risk assessments based on promotional offers and market competitiveness, making the process both dynamic and multifaceted.

Another aspect that intertwines with these considerations is the broader context of market dynamics which often has ripple effects on premium calculations. For instance, recent reports on trends in trailer orders have suggested that fluctuations in freight demand and changes in trucking economics can have subtle yet significant impacts on insurance pricing strategies. When market conditions shift—whether due to seasonal trends, regulatory changes, or economic cycles—insurance providers might update their pricing models accordingly. Such scenarios often lead to scenarios where an internal comparison of policies becomes even more advantageous. Interested readers might explore further insights into these market trends by checking out a detailed analysis on how trailer orders impact truckload margins, which provides a real-world look into how market dynamics interact with insurance economics.

The landscape of commercial truck insurance is continuously evolving as regulatory frameworks adapt to technological advancements and changing safety standards. As policies adjust, the combination of mandatory coverages and optional enhancements creates a complex matrix of pricing that is best navigated with careful planning and informed decision making. Considering that even small adjustments in any of the underlying factors can lead to significant variations in premiums, the process of securing the appropriate insurance coverage becomes an exercise in balancing necessity against cost. In practice, fleet managers need to be vigilant, systematically reviewing their current insurance arrangements and comparing them with emerging offers in the market. This dynamic approach is required not only to safeguard assets but also to remain competitive in an industry where operational margins are often slim.

Technological advancements are also reshaping how insurers assess risk. For instance, telematics and fleet management software now allow for real-time monitoring of driving behavior, vehicle performance, and route optimization. These innovations enable insurers to tailor premiums more accurately, rewarding safe driving and maintenance practices with reduced rates. In this technology-driven environment, fleet operators who invest in the latest monitoring systems may find that their insurance premiums decrease as a direct benefit of improved risk profiling. The data collected from such systems also empowers businesses to implement targeted training programs and adhere to stricter maintenance schedules, which together contribute to a safer operating environment. In the long run, these measures not only enhance operational safety but also prove beneficial in lowering insurance costs. As digital tools increasingly become part of the insurance ecosystem, both insurers and insured parties benefit from a more refined approach to risk assessment.

The importance of holistic risk management cannot be overstated in this context. Insurance premium adjustments are not solely based on static factors like vehicle age or location; they are also influenced by dynamic elements such as the frequency of accidents and claims history over time. A single claim on record may be seen as an outlier, but multiple incidents inevitably signal deeper operational risks. Insurers typically respond to such patterns by recalibrating their pricing models to reflect heightened risk levels. Therefore, businesses that prioritize proactive risk management are likely to witness a more favorable insurance pricing trajectory. Initiatives such as regular driver training, periodical vehicle inspections, and the adoption of advanced safety technologies are all strategies that yield long-term benefits. They not only reduce the likelihood of claims but also enhance the overall reliability of the fleet, resulting in improved safety metrics and lower premiums over successive policy periods.

Moreover, the interplay between economic cycles and insurance costs introduces an additional layer of complexity. In times of economic slowdown or market instability, insurers may tighten underwriting criteria, leading to more conservative premium estimates. Conversely, during periods of economic growth, competitive pressures may drive providers to offer more attractive rates to capture market share. The cyclical nature of the economy thereby reinforces the need for businesses to revisit their insurance arrangements periodically. This review process ensures that premiums remain aligned with the current economic environment and that coverage remains comprehensive relative to the evolving operational landscape.

Furthermore, regulatory agencies and industry bodies play an influential role in shaping insurance pricing standards. In the realm of commercial truck insurance, entities such as the China Insurance Association provide official guidelines that help standardize premium calculations and ensure a level playing field for all market participants. These guidelines serve as an important reference point for both insurers and insured parties, reinforcing transparency and encouraging competitive practices within the marketplace. For those seeking detailed information and the official premium calculation guide, the China Insurance Association’s resource, China Insurance Association – Official Premium Calculation Guide (2026), stands as a reliable external reference that corroborates many of the discussed factors.

In essence, the overall cost of commercial truck insurance is the culmination of a broad spectrum of interrelated variables. It encapsulates risk evaluation based on vehicle type and operational use, the geographical nuances that alter risk profiles, and the behavioral patterns reflected in driver history and claims records. Additionally, the layering of various coverage options, combined with market forces and regulatory guidelines, creates a complex but manageable structure for determining premiums. For those operating within the transportation sector, understanding these cost elements is not only about compliance but also about optimizing overall operational efficiency and financial prudence.

The decision-making process in selecting the right insurance coverage involves a series of strategic choices influenced by both macroeconomic trends and micro-level operational details. Insurers continue to refine their models by integrating real-time data and emerging technologies. This continuous evolution in underwriting practices means that today’s commercial truck insurance policies are more responsive and customized than ever before. Fleet operators who keep abreast of these changes and adopt proactive risk management measures will be better positioned to negotiate favorable terms and secure adequate coverage at competitive prices.

While the nuances of commercial truck insurance may seem daunting at first glance, they offer an invaluable framework for understanding the interplay between risk mitigation and cost control. Operators must navigate a landscape where individual elements such as vehicle type, business purpose, regional factors, and driver behavior converge in a manner that both shapes and is shaped by market dynamics. These factors, taken together, create a pricing architecture that is as much about strategic risk management as it is about regulatory compliance. With careful analysis and a methodical approach, it is possible to unlock significant savings and enhance the overall operational resilience of a fleet.

In conclusion, the detailed examination of commercial truck insurance pricing reveals a multifaceted and dynamic discipline that demands attention to every operational detail. A truck owner or fleet manager who appreciates the significance of elements like vehicle size, usage patterns, location, driver history, and additional coverage options can gain a critical edge in negotiating premiums and managing expenses effectively. The journey toward financial optimization in this sector is paved with continuous learning, strategic planning, and the judicious use of available resources. By embracing a comprehensive approach—where technology, rigorous risk management, and market insights converge—industry participants can ensure that they not only meet regulatory necessities but also derive maximum value from their insurance investments.

Navigating these waters requires diligence and a forward-thinking mindset. It is a process that necessitates revisiting insurance policies periodically, comparing provider quotes, and staying informed about regulatory updates and market trends. This integrated strategy ultimately serves to safeguard assets, boost operational efficiency, and secure competitive premiums. As businesses face evolving challenges and opportunities, maintaining a robust framework for assessing and managing insurance costs will remain a crucial aspect of strategic decision making in the commercial trucking industry.

Navigating the Complex Web of Variables Behind Commercial Truck Insurance Costs

Commercial truck insurance cost is not determined by a single factor, but rather by a complex interplay of several elements that influence overall premiums. Every operator, whether a new owner or an established fleet manager, encounters a unique set of circumstances that shape the final cost, and understanding these variables can provide a clearer picture of what to expect when securing insurance coverage for commercial trucks. At the forefront of these factors is the driver profile, which is critical in assessing risk. The age, level of experience, and past driving record of the truck operator directly affect insurance premiums. Newer drivers or those without extensive experience typically face higher rates because insurance companies view them as having a higher risk of accidents or claims. Similarly, a history marked by multiple traffic violations or a record of accidents pushes the insurer to raise premiums, reflecting anticipated increased costs down the line. Even within experienced driver groups, subtle differences such as driving habits and frequency of long hauls may adjust the premium amount. This interconnectedness of risk and responsibility has driven insurers to closely monitor driving records and provide incentives for those who exhibit safe driving behaviors over time.

The characteristics of the vehicle itself play an equally significant role in determining premiums. Commercial trucks vary widely not just in size and capacity, but also in terms of their technological features, physical condition, and even specialized modifications. A truck used for long-haul routes, for instance, presents a different risk profile compared to one used purely for local or regional deliveries. Newer, high-value vehicles often incur higher insurance costs since their replacement value and repair expenses tend to be much higher than older, depreciated models. Trucks fitted with advanced safety features or specialized equipment such as refrigeration units for perishable goods might initially appear to command a premium, yet in some cases, these features may lower risk by reducing the probability or severity of accidents. Moreover, the normal usage of a vehicle—whether it is for short urban errands or extended interstate journeys—can significantly alter its risk exposure, thereby impacting the premium. Fire, theft, and collision coverages, which are often chosen based on vehicle type and value, add another layer of cost that must be carefully balanced against the operational needs and financial security of the business.

Another crucial determinant in commercial truck insurance pricing is the operating environment, which includes geographical and operational considerations. Trucks operating in densely populated urban centers, where congestion and a high rate of accidents are common, experience inherently higher risks compared to vehicles operating in rural or less trafficked regions. Urban areas usually have more complex traffic patterns, higher likelihoods of theft or vandalism, and stricter local regulations—all of which can drive up the cost of insurance. Conversely, trucks that predominantly operate in areas with lower traffic density might benefit from reduced premiums because of the relatively easier operating conditions and lower accident risks. Notably, local regulatory environments can also change with shifting political landscapes or evolving traffic safety standards, making it essential for fleet managers and individual operators alike to remain current with regional policies. This dynamic nature of geographic influences means that even if a driver or fleet has maintained a pristine record, the cost of insurance may still fluctuate based on their operational base or typical route profiles.

Coverage choices and claims history add further dimensions to the overall cost structure of commercial truck insurance. Operators have the option to tailor their policies with various coverages ranging from standard third-party liability to more comprehensive protections including physical damage, cargo, theft, and passenger liability. Deciding on the right mix involves weighing potential risks against the premium cost, and selecting additional coverages inevitably increases the base price. How comprehensive the coverage is becomes especially important for businesses that transport high-value goods, where the added protection mitigates potential financial losses in the event of an accident. Furthermore, an operator’s historical claims record is a strong determinant of policy pricing. Those with a history of frequent claims or costly payouts often see their premiums increase, a reflection of the insurer’s assessment of risk based on past performance. On the other hand, drivers or companies that have maintained a clean claims history benefit from lower premiums, sometimes earning additional incentives such as discounts or favorable rating adjustments.

Even beyond the individual characteristics of drivers and vehicles, the methodologies employed by different insurance companies contribute to premium variations. Each provider utilizes its own set of underwriting criteria and risk models to arrive at pricing structures that reflect broader market trends as well as internal risk assessments. Since the implementation of reforms in auto insurance rating systems, notably those introduced around 2021, insurers have increasingly factored in elements such as base premiums and No Claim Discounts (NCD) when setting rates. This diverse range of pricing models means that two operators with seemingly similar profiles might receive differing quotes from separate providers. Navigating these discrepancies requires careful research and comparison shopping, as even marginal differences in underwriting approaches can translate into significant cost differences over the term of a policy. Furthermore, some insurers offer promotional rates or incentives aimed at specific driver demographics, or for operators who consistently demonstrate safe and prudent driving habits. In this competitive marketplace, selecting the right insurance partner can be as crucial as the individual risk factors that are assessed.

While the above factors account for many of the influences on commercial truck insurance rates, several other considerations also add nuance to the pricing landscape. The ever-changing economic environment plays a non-negligible role. Fluctuations in the market value of trucks, variations in repair and parts costs, and even changes in fuel prices can indirectly affect the cost of insurance. For instance, if repair costs spike due to higher parts prices or advanced technology in newer trucks, the overall risk exposure for insurers increases, leading to higher premiums. Insurance companies, therefore, must constantly update their risk models and adjust rates to reflect these economic realities. Similarly, every operator must remain aware of how business cycles and broader market conditions impact the trucking industry, as a downturn in the economy might offset premium costs by leading to fewer claims when overall traffic decreases, while a booming economy might bring increased premiums in tandem with more active transportation networks.

Another element that sometimes escapes notice is the cumulative impact of multiple smaller risk factors which, when aggregated, significantly affect overall costs. Minor infractions by drivers, infrequent but costly repairs due to vehicle wear and tear, and even the occasional incident in the operating environment can add incremental risk that insurers must account for. Even if no single small factor appears significant on its own, the combined risk can raise the overall cost structure of the policy. This cumulative effect means that every aspect of the operation, from rigorous vehicle maintenance schedules and proper driver training programs to efficient route planning, contributes indirectly to the final tally of insurance expenses. In many cases, proactive measures can help reduce these accumulated risks. Operators who invest in regular training for their drivers, implement robust safety protocols, and use modern technology to monitor vehicle performance often enjoy the benefits of lower premiums, as their well-documented risk mitigation strategies reassure insurers of a reduced chance of future incidents.

In the context of maintaining a competitive edge in a rapidly evolving industry, fleet operators are increasingly finding that optimizing operational practices is essential not just for daily efficiency but also for long-term financial planning. The strategies adopted by fleets to manage costs extend far beyond simply looking up premium rates. Many have begun integrating continuous risk management practices and leveraging data analytics to predict and even preempt potential incidents before they occur. For instance, advanced telematics systems offer real-time insights into driver behavior and vehicular performance, allowing network operators to swiftly implement corrective measures. This proactive approach does not just enhance safety; it directly contributes to lower insurance premiums. Insurance providers are recognizing these advancements and, as a result, are increasingly offering discounts to fleets that implement cutting-edge safety and monitoring technologies. As the industry evolves, embracing technological innovations and operational best practices becomes even more critical in managing and optimizing insurance costs.

The interplay between internal management practices and external market conditions is further complicated by regulatory influences that affect the insurance landscape. In many regions, there are mandatory coverage requirements that form the baseline for any commercial truck insurance policy. These compulsory coverages ensure that all operators have a minimum level of protection against common risks. However, the level of mandatory coverage can vary significantly from one jurisdiction to another. In some cases, operators may be required by law to hold policies that provide more comprehensive protections, leading to higher baseline costs. In other regions, there might be more flexibility, allowing operators to tailor their policies more finely to their specific risk profiles. This regulatory framework not only adds another layer of complexity to the cost but also means that insurance providers must operate within tightly defined legal boundaries when setting their rates. In this context, staying informed about current and upcoming regulatory changes becomes an integral part of managing commercial truck insurance expenses.

Balancing the need for comprehensive coverage with the goal of minimizing unnecessary expenses is a challenge that all fleet managers must tackle. One effective strategy is the deliberate selection of coverages that are most pertinent to the operation. For example, a company that relies on the safe and timely delivery of cargo may place a premium on cargo insurance, while another operator, whose trucks frequently navigate high-risk urban environments, may opt for more robust liability coverage. In some cases, operators choose to forgo certain extras in favor of lower premiums if their operations support a lower risk profile or if they have managed to secure additional risk mitigation measures independently. This balancing act requires a nuanced understanding of both the short-term benefits and the long-term implications of various coverages. Comparing different policy options side by side, and often consulting with multiple insurance providers, can help companies land on a policy that not only fits their immediate budgetary constraints but also aligns with their long-term operational strategies.

A particularly challenging aspect of determining commercial truck insurance cost lies in the unpredictable nature of risk and how it intersects with human factors. Even with sophisticated modeling and vast amounts of data, insurance pricing remains sensitive to unforeseen events. Natural disasters, sudden shifts in economic conditions, or unexpected regulatory changes can all rapidly alter the risk landscape. In such circumstances, what might once have been considered an outlier becomes part of a broader statistical trend that impacts premium calculations. The precarious balance between statistical risk and real-world variability ensures that both insurers and insured parties must remain vigilant and adaptable. In many cases, building a buffer into financial planning for unexpected insurance cost increases is prudent, allowing operators to manage occasional spikes in cost without destabilizing their overall budget.

Beyond the immediate financial considerations, commercial truck insurance is also intertwined with the broader operational health and sustainability of a business. For many organizations, particularly those that form the backbone of supply chains, the ability to secure insurance is not only a legal obligation but a critical component of sustaining profitable operations. Expensive accidents or unanticipated incidents can quickly destabilize an operation, making insurance not just a protective measure, but a cornerstone of strategic planning. Fleet operators must therefore view insurance as an investment—a necessary safeguard that, when managed well, paves the way for business continuity and resilience in the face of unforeseen challenges. This perspective encourages a holistic approach to risk management, wherein every element of operation, from driver training and vehicle maintenance to regulatory compliance and financial planning, is considered in tandem with insurance strategy.

The evolving landscape of commercial truck insurance costs requires operators to continually adapt and reassess their strategies. For instance, as technological advances continue to reshape the transportation industry, traditional risk factors are being supplemented with new dimensions of data and analytics. Innovations in real-time tracking, vehicle diagnostics, and even artificial intelligence-driven predictive maintenance are enabling operators to forecast risk more accurately. In many respects, this digital transformation is not only enhancing operational efficiency but also compelling insurers to refine their underwriting processes. This convergence of technology and finance means that operators who are quick to adopt new tools may find themselves rewarded with lower insurance premiums, as their enhanced risk management capabilities translate into lower probabilities of untoward incidents. Embracing such technologies, however, requires an upfront investment and a commitment to continuous improvement—a challenge that many modern fleet managers are increasingly prepared to meet in order to stay competitive in a rapidly changing market.

A robust understanding of these dynamics can be bolstered by engaging with industry insights and expert commentary. For example, discussions on trends such as capacity fluctuations within the trucking market can provide valuable context and highlight the economic underpinnings that affect insurance costs. For those interested in how market conditions play a role in pricing trends, insights available in resources like the analysis on excess capacity in the trucking market can serve as an informative supplement to direct insurance considerations. By integrating data from such specialized analyses, operators can form a more comprehensive view of the challenges and opportunities that lie ahead. Additionally, staying updated with periodic reports and guidelines issued by reputable institutions, such as the National Association of Insurance Commissioners (NAIC), ensures that both individual operators and large fleets remain informed about the regulatory and economic forces at work.

In conclusion, understanding the multiple variables that shape commercial truck insurance costs requires a careful analysis of driver profiles, vehicle characteristics, operating environments, coverage choices, and the pricing methodologies employed by insurers. The synthesis of these elements into a coherent understanding helps to ensure that operators can navigate the complex and dynamic nature of insurance costs, making informed decisions that balance risk with financial prudence. Maintaining a clear perspective on these factors not only aids in optimizing insurance expenditures but also fortifies the strategic operations of a transportation business. Through continued vigilance, technological adoption, and adaptive risk management, fleet operators can achieve a balance that facilitates sustainable growth while safeguarding against unforeseen financial burdens. For further insights into the varied influences on insurance rates and the broader economic context, one resource to consider is the comprehensive review presented in recent discussions on excess capacity in the trucking market insights. By aligning operational practices with these broader trends, operators can position themselves to tackle the inevitable challenges of modern commercial trucking with a well-informed, strategic approach.

Ultimately, the cost of commercial truck insurance remains a subject of continuous evolution, intricately tied to factors both within and outside of an individual operator’s control. Maintaining an informed stance means regularly reviewing all aspects of one’s risk profile while staying attuned to external economic and regulatory shifts. As the transportation industry continues to innovate and expand, the interplay between traditional risk factors and new technological advancements will further redefine the landscape of insurance. In navigating this multifaceted terrain, operators who invest in comprehensive risk management strategies not only shore up their operational resilience but also stand to benefit from increasingly tailored and competitive insurance solutions. This ongoing balance of risk, cost, and strategic investment is essential for any business seeking long-term stability in a field where the unexpected is not the exception, but the norm.

Navigating the Labyrinth: Unraveling the Pricing Structures Behind Commercial Truck Insurance in 2026

Commercial truck insurance is a complex and evolving landscape that requires careful navigation by truck owners and fleet managers alike. In 2026, the average premium fluctuates significantly with factors ranging from vehicle type and driver history to the level of coverage selected and emerging safety technologies. A closer look at these pricing structures reveals that while standard coverage may cost between $80 and $150 per month, additional variables such as hazardous material transport, fleet size, and advanced telematics integrations can push monthly premiums to over $300 per truck. Understanding this intricate web of pricing determinants is essential for those seeking not only to manage their operating expenses but also to secure reliable coverage that suits the exact needs of their business operations.

At the heart of commercial truck insurance pricing is the type and size of the vehicle. Trucks are not a one-size-fits-all commodity; instead, they range from light-duty vehicles weighing between one and five tons to heavy-duty tractor-trailers or specialized units such as refrigerated, tanker, or electric vans. Lighter vehicles often enjoy lower premiums due to their reduced risk profile and lesser repair costs, whereas heavy trucks or those carrying hazardous materials tend to incur higher rates due to the increased likelihood and potential severity of claims. For example, a single-truck owner-operator with a light-duty vehicle might secure a policy within the $80 to $100 per month range if they maintain a clean driving record and invest in safety technology. Conversely, fleets involved in long-haul operations that transport volatile cargo are likely to examine options that exceed $300 per month per truck because of the added risk factors. The inherent differences in vehicle design, usage intensity, and operational risk mean that pricing is customized rather than standardized, demanding that policyholders closely assess their individual circumstances before committing to a coverage plan.

Coverage levels are another pivotal element in determining commercial truck insurance premiums. A basic liability policy, which might include the mandated third-party liability similar to compulsory traffic insurance in some regions, is generally the most economical choice. However, many operators opt for comprehensive policies that incorporate physical damage, cargo coverage, non-owned auto liability, and even specialized endorsements like theft protection and passenger liability. With each additional coverage feature, insurers factor in the likelihood of claims as well as the potential costs associated with repairs or replacements. For instance, vehicle damage insurance might cost between $5,000 and $6,000 per year for a new vehicle, with rates adjusting downward over time as the truck depreciates. Cargo insurance also introduces variability as premiums are influenced by cargo value and shipment frequency, thereby adding layers of intricacy to the overall pricing structure. This interplay between mandatory and optional coverages pushes premiums to levels that may fluctuate notably from one insured entity to the next.

Moreover, driver history and fleet management practices play an indispensable role in shaping insurance costs. A driver with a spotless record, free from accidents, DUIs, or moving violations, can see a reduction in premium costs by as much as 30%, while a history of claims or traffic infractions can cause insurers to adjust rates upward. Fleet managers who implement robust safety programs and advanced driver training sessions typically experience fewer claims, thereby benefiting from lower premium rates. Additionally, companies that manage larger fleets often enjoy bulk discounts or savings programs engineered around fleet management tools. Programs offered by various insurers provide real-time monitoring and analytics that not only enhance driver safety but also yield significant financial benefits through reduced premiums. Some providers offer discounts of up to 40% when such safety technology is integrated, underlining the importance of both individual and collective risk mitigation strategies in the commercial truck insurance space.

Geographic location adds another layer of complexity to the pricing equation. Urban areas with high traffic density, frequent congestion, and elevated accident rates tend to yield higher premiums compared to rural regions where the risks are relatively lower. Insurers take into account local accident statistics, theft rates, and even weather patterns when calculating rates. A truck operating in a major metropolitan area might face a premium on the higher end of the spectrum to account for the increased likelihood of incidents, while trucks operating in less congested areas may be rewarded with lower costs. This geographic risk is further influenced by regulatory standards, as different states or countries may impose divergent coverage requirements that directly affect the premium amount. Hence, truck owners must recognize that the environment in which they operate not only impacts operational risks but also significantly sways insurance costs.

The integration of telematics and other safety technologies has emerged as a game-changing factor in the realm of commercial truck insurance. Modern systems that monitor real-time driving behavior—such as speed, braking intensity, and cornering—are quickly becoming standard practice among insurers looking to precisely assess and manage risk. Drivers who agree to use such equipment can benefit from tangible discounts on their premiums, as the data collected serve as evidence of safer driving practices and lower accident probabilities. This technological revolution in insurance isn’t merely about data collection; it represents a holistic approach that combines driver accountability with advanced risk management. Insurers are increasingly incentivizing the use of these tools, recognizing that a well-monitored driver is less likely to engage in risky behavior. Thus, the adoption of telematics has become a cornerstone in driving down insurance costs while simultaneously promoting a culture of safety and responsibility on the roads.

Adding to the complexity is the matter of insurance providers’ differing pricing models and promotional offers. Companies like Geico and USAA, for instance, may present special discounts for driver groups with exemplary performance records or for individuals affiliated with the military. Meanwhile, other insurers may structure their pricing with a focus on comprehensive coverage bundles that incorporate multiple facets of risk management. Because each insurer approaches risk assessment and premium determination uniquely, it becomes imperative for fleet operators and owner-operators to engage in extensive market research before finalizing a policy. The importance of obtaining customized, detailed quotes tailored to the specific details of the truck, its usage, and the geographical operating area cannot be overstated. This competitive environment among insurers ensures that there is no one-size-fits-all pricing strategy, further emphasizing the necessity for due diligence in the selection process.

An additional factor that influences pricing is the age and condition of the commercial truck. Newer vehicles typically attract higher premiums due to their higher replacement value and the increased costs associated with repairing modern technology and sophisticated safety systems. However, as a truck ages, its value diminishes and so does the potential payout risk for the insurer, resulting in lower premium costs. This depreciation effect means that operators with older trucks may find themselves in a more favorable position when negotiating terms, provided that the vehicle is still maintained in compliance with safety standards. Conversely, even a well-maintained new truck may command a premium that seems steep relative to an older model due to the inherent pricing models built into insurance calculations. Understanding the relationship between vehicle age, value, and subsequent insurance costs is crucial for those trying to either upgrade their fleet or extend the operational life of existing assets.

Furthermore, the specific operational needs of a business have a significant impact on insurance rates. Companies that transport high-value or hazardous cargo often find themselves paying higher premiums due to the elevated risk associated with the potential for costly claims or environmental damage. The increased scrutiny from insurers in such sectors is well justified, as even a single incident involving hazardous materials can lead to catastrophic financial and reputational damage. Consequently, businesses that fall into these specialized categories may see their insurance premiums soar, prompting them to invest heavily in risk mitigation strategies and advanced safety protocols. On the other hand, operators who stick to less risky cargo types and maintain rigorous safety standards tend to benefit from more competitive pricing structures, further highlighting the role of operational strategy in premium determination.

The need for competitive pricing and efficient risk management has also led insurance providers to offer innovative programs aimed at rewarding safer driving and better fleet management. For instance, some industry players offer programs that directly link safe driving metrics with premium reductions. These programs not only encourage better driving habits by providing immediate financial incentives but also reinforce a broader culture of accountability within the trucking industry. Companies that participate in such initiatives often report a noticeable decline in the number and severity of claims, reinforcing the idea that prevention is both a safety measure and a financial strategy. By leveraging advanced monitoring tools and targeted training programs, fleet operators can drive down costs while simultaneously enhancing operational efficiency. This blend of technology and proactive safety management illustrates the dynamic interplay between regulatory compliance, technological innovation, and economic pragmatism in commercial truck insurance.

In addition to these factors, it is increasingly common for truck operators to face variations in premium amounts depending on how many trucks are insured under a single policy. Fleet discounts become particularly attractive for large-scale operations, where volume can translate to significant savings. Insurers view a large, well-managed fleet as a lower risk per individual unit due to the likelihood of shared safety protocols and consistent maintenance standards across vehicles. This bulk discount approach not only reduces the per-truck premium but also simplifies administrative processes by consolidating coverage under one provider. Yet, the flip side of this arrangement is that smaller operators or owner-operators may not have access to such savings, meaning that individual quotes are likely to be comparatively higher. Recognizing the economies of scale and the benefits of comprehensive fleet management is therefore essential for all operators striving for cost efficiency when navigating the commercial truck insurance market.

Throughout this intricate pricing mosaic, the role of market competition and varied promotional offerings cannot be ignored. The insurance market is marked by a wide range of providers, each with their own unique approach to estimating risk and setting rates. This competitive atmosphere has led to a situation where individualized offers—sometimes as low as $42 per month for exceptional risk profiles—appear alongside more standard premium ranges. Such variations underscore the importance of proactive engagement with multiple providers to secure the most favorable terms available. Operators are encouraged to frequently revisit available quotes, especially as their operational profile evolves or as technological enhancements in vehicle safety are adopted. This continuous process of assessment and reassessment is key to maintaining an optimal balance between comprehensive coverage and budgetary constraints in an environment that is as dynamic as it is competitive.

When companies take into account these multifaceted factors, it becomes evident that obtaining the best possible commercial truck insurance is not merely a matter of selecting a policy off the shelf. Instead, it calls for a strategic approach that factors in truck type and size, coverage levels, driver behavior, geographic risk, and the evolving landscape of technology and fleet management. Each element influences the overall pricing in a meaningful way, and a failure to consider one or more of these aspects can result in unexpected costs down the line. In this way, commercial truck insurance operates on multiple levels, each interacting to form a pricing structure that, while daunting at first glance, can be deciphered with careful analysis and timely action. For those invested in staying ahead in the market, it is advisable to periodically review available discounts and to update safety measures that contribute to long-term reductions in premium amounts.

In certain cases, the intricacies extend even further. Many operators have observed that seasonal trends and fluctuating market conditions may also impact commercial truck insurance costs. During periods of high demand, profitability margins may shrink for insurance providers, prompting them to adjust quotes upward. Conversely, in a more competitive market with an oversupply of service providers, rates may be driven down as companies vie for business. These shifts can often be unpredictable, requiring operators to remain ever-vigilant about industry trends and broader economic indicators. When contextualized within the larger framework of market dynamics, these seasonal and economic factors illustrate that the pricing of commercial truck insurance is as much a reflection of macroeconomic trends as it is of individual risk factors.

For operators looking to gain additional insight into how these market trends and pricing adjustments are managed on a broader scale, it is worth exploring detailed analyses of related economic factors. In fact, resources that address shifts and challenges in the trucking industry – spanning topics from cross-border regulatory challenges to macroeconomic impacts on trucking margins – prove invaluable. Interested readers can delve into further discussion on sector-specific economic fluctuations by reviewing insights on recent industry developments, such as those found in studies on trailer market trends. In many ways, the nuances of commercial truck insurance pricing reflect these broader trends, offering a window into how regulatory measures, safety advancements, and market competition all converge to influence costs.

It is also important to recognize that while one might fixate on monthly premiums or base costs, the true value of commercial truck insurance extends beyond the price tag. This value is best assessed through the lens of long-term operational stability and the financial protection it affords against unforeseen risks. After all, even the most competitive premium cannot compensate for the potential fallout from an inadequately covered claim. Ensuring that the insurance policy not only meets the immediate financial requirements but also provides robust protection in the event of an accident or incident is critical. This comprehensive view emphasizes that insurance is an investment in continuity and reliability, safeguarding the future of business operations against the unpredictable nature of the road.

Ultimately, the journey toward obtaining the most cost-effective and comprehensive commercial truck insurance policy is one defined by its complexity and its reliance on a blend of quantitative metrics and qualitative assessments. Trucking professionals must remain adaptable, proactively seeking out updated quotes and new risk management technologies that offer both immediate and long-term cost benefits. As market conditions evolve and new safety standards emerge, the pricing structures themselves will continue to undergo transformation, necessitating ongoing attention and strategic decision-making. For those willing to invest the time and effort to understand every dimension of this multifaceted process, the rewards can be significant – a robust insurance policy that not only meets regulatory requirements but also bolsters the overall financial health of the operation.

In closing, while the cost of commercial truck insurance in 2026 may initially appear daunting due to its myriad influencing factors, careful evaluation reveals that it is ultimately a manageable element of overall business strategy. Truck owners and fleet managers are empowered by a range of options that allow them to tailor their coverage precisely to their needs, thereby striking an optimal balance between cost-efficiency and comprehensive protection. The interplay between vehicle type, coverage options, driver history, geographic considerations, and modern safety technologies creates a dynamic pricing environment that rewards diligence and strategic planning.

For those tasked with navigating this complex terrain, the key takeaway is that knowledge and preparation are the best defenses against unforeseen expenditure. Armed with a detailed understanding of each pricing factor, operators can seek out targeted discounts and employ cost-saving measures that collectively lead to substantial savings over the course of a policy term. It is this proactive and informed approach that ultimately enables business owners to secure reliable protection without overextending financial resources. As the industry continues to evolve, staying abreast of the latest trends and innovations remains paramount, and ongoing monitoring of both internal practices and external market conditions is essential for long-term success.

For further official guidance and a deeper understanding of how these factors interact within a regulatory framework, readers are encouraged to consult trusted, external resources such as the comprehensive insights provided by the National Association of Insurance Commissioners (NAIC).

Final thoughts

In summary, the landscape of commercial truck insurance is intricate, shaped by numerous elements ranging from the type and size of the vehicle to geographical risks and individual driving records. Logistics and Freight Company Owners, Construction and Mining Enterprises, and Small Business Owners with Delivery Fleets must consider these factors carefully to understand their insurance costs fully. Knowledge of average pricing can empower decision-makers and can lead to better financial planning and operational efficiency.